Tracy

TracyThe recent US Supreme Court ruling will reduce Sri Lanka’s overall tariff from about 31% to 21.6%, with apparel seeing nearly a 10‑point cut.

More Sri Lankan products now qualify for tariff exemptions, granting additional-tariff‑free access for USD 65 million worth of exports.

The potential for additional tariff reductions via framework agreements with the US is limited since the existing agreements have produced only small tariff reductions.

The US Supreme Court struck down tariffs imposed under the International Emergency Economic Powers Act (IEEPA) on 20 February 2026, creating uncertainty about future US tariff policies. The US has used IEEPA to impose reciprocal tariffs on trade partners and additional fentanyl-related trade measures for Canada, China, and Mexico since 2025. At the time of the Supreme Court ruling, Sri Lanka’s reciprocal tariff rate was 20%. The US administration quickly invoked Section 122 of the Trade Act of 1974 to maintain high tariffs. Section 122 allows a US president to address international payment issues.

Moving forward, Sri Lanka will face three different tariffs: namely, 1) 10% Section 122 tariff, 2) the Section 232 tariff, and 3) the Most Favored Nation (MFN) tariff. Notably, the Section 122 tariffs are only valid for 150 days, and the US has signalled that this rate will rise to 15%. Amid these developments, this article analyses how the US Supreme Court judgement affects tariffs faced by Sri Lanka, and Sri Lanka's relative tariff position vis-à-vis competitors like Indonesia, Cambodia, and Bangladesh.

How has the tariff changed since ‘Liberation Day’?

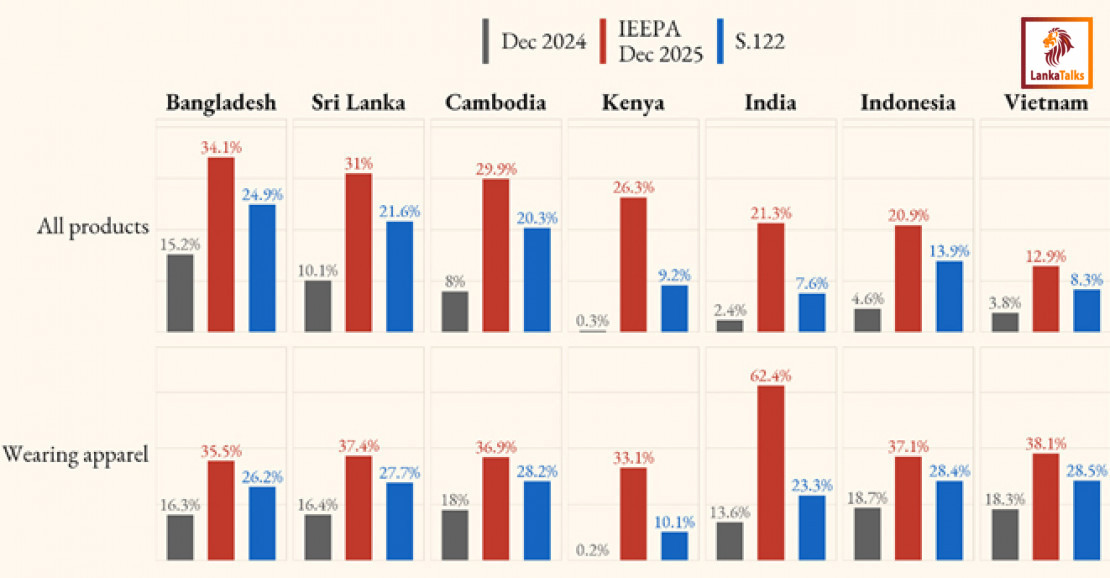

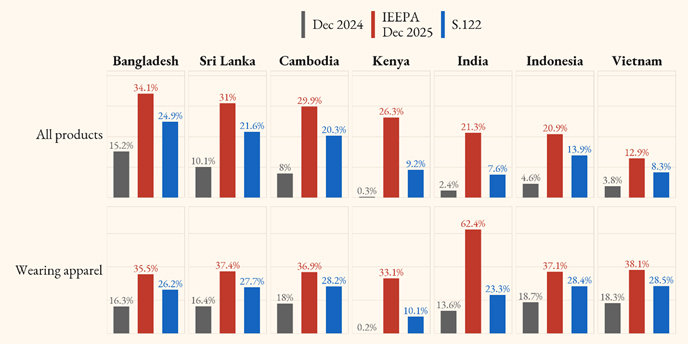

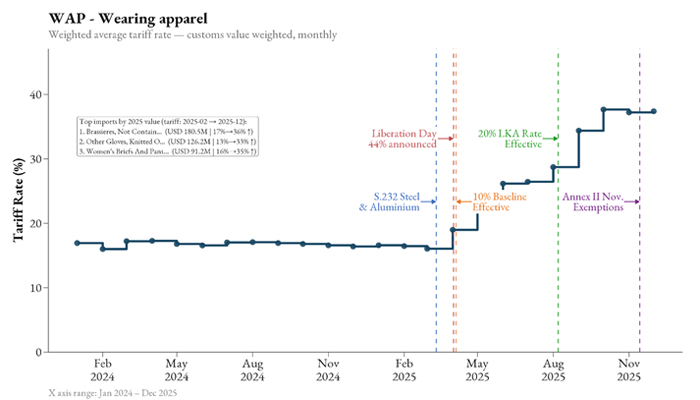

The ‘Liberation Day’ tariffs introduced in 2025 gradually raised Sri Lanka's effective tariff rate in the US. By the end of December 2025, IEEPA and Section 232 tariffs were fully implemented, increasing the US effective tariff rate on Sri Lanka by 21% (Figure 1). The effective tariff rate on wearing apparel products increased to 37.4% in December 2025 for Sri Lanka from 16.4% a year ago. Sri Lanka’s competitors in the US market also saw a similar tariff increase. India experienced a 49% tariff increase following the imposition of a 50% tariff (Figures 1 and 2).

Figure 1: Evolution of effective tariff rates: from MFN to Section 122

Source: Author’s calculations using DataWeb, USITC

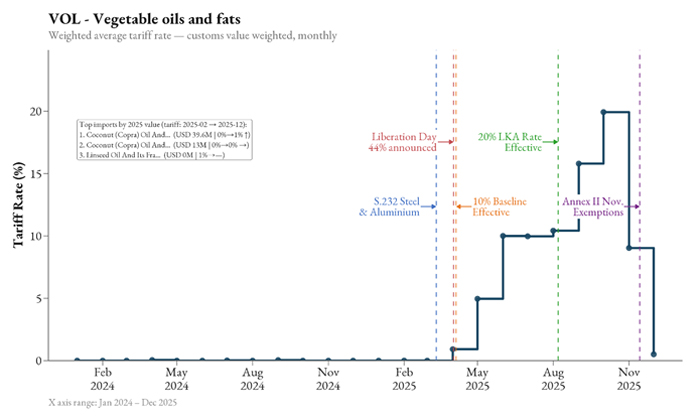

The tariff rise was not uniform due to exemptions and section tariffs, such as those on steel and aluminium. In November 2026, the US expanded these exemptions to include agricultural products. The notable beneficiary of this exception was Sri Lanka's coconut oil exports (Figure 3). The effective tariff rate plummeted to the MFN level in November, resulting in a close-to-zero rate. In contrast, steel- and aluminium-related products saw a tariff increase of nearly 40 percentage points due to the Section 232 tariff, which was set at 50%.

Figure 2: The US tariff movement on Sri Lanka’s wearing apparel exports: January 2024 to December 2025

Source: Author’s illustration

Figure 3: The US tariff movement on Sri Lanka’s vegetable oils and fat exports: January 2024 to December 2025

Source: Author’s illustration

Current US tariff regime: Comparative analysis

Even after rescinding the IEEPA tariffs, the Section 122 tariff system will remain complex as exemptions and sector-specific tariffs will continue for products such as steel, aluminium, copper, and auto parts. However, Sri Lanka’s exposure to these tariffs is limited, although they affect certain manufactured products.

The US will also continue to seek a sustainable legal basis for imposing higher tariffs, as indicated by various communications. The US-proposed Turnberry System uses tariff as a “formidable stick” to motivate compliance, because it lacks a formal dispute settlement mechanism. The ability to impose and maintain high tariffs is essential for the US to sustain the proposed system. Given that the Section 232 tariffs have withstood legal challenges, it is likely that additional tariffs will follow under this section. The United States Trade Representative also expressed the intention to initiate several Section 301 investigations. The Section 301 tariffs are designed to address “unfair” trade practices, a tool used in the China-US trade war in 2018.

Using the December 2025 export basket, the impact of the current US tariff regime can be estimated. The current Section 122 rate is 10% and it is applied on top of the base MFN rate. Products are exempt from the 10% tariff when Section 232 is applied. Under the Section 122 tariff regime, Sri Lanka's effective tariff rate will fall to 21.6% from 31.0%. A similar reduction applies to Cambodia and Bangladesh. India’s effective rate will decline by 13.7 percentage points. As Section 122 and the reinstatement of the African Growth and Opportunity Act (AGOA) are likely to take effect simultaneously, Kenya’s effective rate will fall to 9.2%, largely because MFN rates would no longer apply. If Section 122 rises to 15%, Kenya will see a tariff increase compared to the IEEPA and AGOA tariff regime.

The Section 122 tariff regime is less harmful to Sri Lanka for three reasons. Firstly, due to the reduction in tariff rates from higher levels under IEEPA (Figure 1). Secondly, it also reduces the tariff gap between Sri Lanka and countries with favourable tariff arrangements under the IEEPA regime. The tariff differential between countries like Kenya goes down. For example, the effective tariff rate for wearing apparel exported by Kenya was about 10% under the IEEPA and AGOA tariff regime, while Sri Lanka faced a 37% rate, creating a 27% tariff gap between the two countries. However, under Section 122, the differential will be about 17%. A similar differential reduction occurs against Canada and Mexico, which are part of the United States-Mexico-Canada (USMCA) free trade agreement. When other countries faced higher reciprocal tariffs, the USMCA preferential premium for Canada and Mexico was higher. The USMCA premium reduction may help countries like Sri Lanka, which export rubber products.

Thirdly, exemptions under Section 122 tariffs cover 546 additional products at the eight-digit level, when compared to the IEEPA exemptions. In 2025, Sri Lanka exported 1,233 unique eight-digit products to the US valued at USD 3,211.6 Mn. Among them, 84 product codes were in the IEEPA exemptions. Sri Lanka exported USD 262.1 Mn, or 8.2% of its total exports, under these exemptions in 2025. However, if the same basket is exported under Section 122, 162 products will be exempt from the Section 122 tariff. In 2025 values, these products were worth USD 327.2 Mn, or 10.2% of Sri Lanka's exports. Accordingly, the Section 122 tariff regime gives free market access to additional USD 65.1 Mn worth of products. Sri Lanka gains zero additional tariffs on 80 products, including articles of vulcanised rubber, rubber bands, transformers, and engine testing equipment.

Policy options for Sri Lanka

Rapid shifts in US trade policy have left Sri Lanka with almost no feasible response. Sri Lanka’s competitors adopted ‘framework agreements’ with the US to eliminate uncertainty. However, the current Section 122 exemptions cover almost all tariff concessions offered through these agreements. Thus, countries have no incentive to grant large concessions to the US, and signatories already demand clarity on the future of these deals.

Sri Lanka can similarly form a framework agreement with the US to secure tariff concessions. Even if such an agreement offers zero tariff concessions on all products listed in “Potential Tariff Adjustment for Aligned Partners,” Sri Lanka will only gain zero tariffs on 60 of its exports, including precious stones and activated carbon. Therefore, any reciprocal agreement should be carefully assessed for its costs and benefits.

Source: Adaderana